After years of macro-driven markets and passive dominance, something important has changed in equity markets.

Dispersion is back.

Dispersion measures how differently individual stocks move relative to one another. When dispersion rises, relationships between correlated stocks temporarily break down—creating the exact inefficiencies that statistical arbitrage strategies are designed to exploit.

And in 2025 and 2026, dispersion surged.

During recent volatility shocks, sector rotations, tariff news and macro news pushed many historically related stocks and ETFs significantly out of alignment. For traders running equity market neutral strategies,

… Read More →

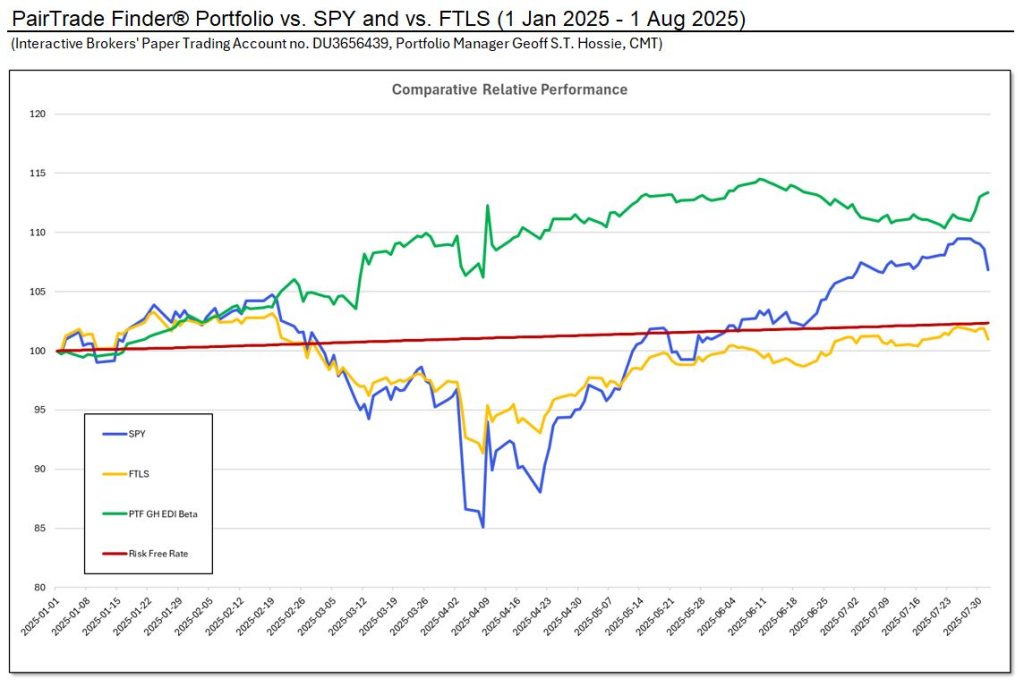

Trade-Level Performance: Precision in Execution

Trade-Level Performance: Precision in Execution